The pension savings dilema

Written by David Liegeois

Event: On September 11, we held a live event with a presentation and discussion on the simulation model, its results and the implications for individual investors in Belgium. You can find the recording just above this text.

Simulation model: You can download or make a copy of the simulation model here.

Should you continue your pension savings plan or invest in index ETFs instead?

A large part of the FIRE community shares the view that investing in tax-advantaged individual pension savings (3rd pillar) is not worth it and that investing on your own through low-cost passive index funds is always a better idea.

The reality is a little more nuanced than that. Depending on a whole series of parameters, including some which depend on the investor’s personal situation, it may in some cases be more attractive to invest in pension savings and obtain a higher amount at the end.

Curvo and Thomas Guenter have carried out simulations comparing the two options (on Curvo website and on the VFB website). But these simulations seem to take into account three hypotheses that penalize pension savings.

- Firstly, the non-reinvestment of the tax advantage. By reinvesting the tax advantage into index ETFs, the return on an investment through pension savings is improved.

- Secondly, pension savings are compared to a 100% investment in stocks. It’s not necessarily always the case. Indeed, a significant part of investors do not want a portfolio with an allocation of 100% stock. It is therefore interesting to compare an investment through pension savings and an investment through ETF composed of an equivalent percentage of stocks/bonds in order to compare 2 portfolios with equivalent risk.

- Finally, the ETF investment is not systematically sold at the end of the simulation, and therefore does not suffer from broker fees, stock exchange transaction tax (TOB) or a possible Reynders tax. For its part, investment through pension savings, which has been subject to an 8% tax at the age of 60 of the investor, is therefore net of taxes after the payment of this tax.

Parameters for pension savings

The different parameters for pension savings are as follows:

- The age at which you start investing. The closer you are to the year you turn 65 (the year in which you can receive the last tax benefit), the more interesting pension savings become, as the simulations show.

- The amount to invest. Pension savings offer two ceilings, the first of which allows a tax advantage of 30% and the second 25% (+municipal tax), i.e. €1,020 and €1,310 respectively.

- The percentage of municipal tax. Depending on where you live, the higher it is, the more it improves the return on your tax benefit.

- Entrance fees. These, between 0% and 3%, and depending on the fund, reduce the return on pension savings.

- Professional status. Employees can benefit from an additional tax advantage in some cases through a flex income plan. Other parameters such as the maximum tax bracket or the conversion factor of the flex income plan will then have to be taken into account.

- The return on pension savings. The annualized return over the last 20 years (2004 to 2023) can range from 2% to more than 6.2%. This return depends mainly on the percentage of stocks and bonds in the fund. The more stocks there are (dynamic fund), the higher the return is assumed to be at maturity.

Parameters for ETF investing

For ETF investing, the parameters are as follows:

- The percentage of TOB. From 0.12% to 1.32%. The higher it is, the lower the yield.

- The broker’s transaction fees for buying and selling the ETF. Just like entry fees, the higher they are, the lower the return.

- The percentage of stocks and bonds in the portfolio. The more stocks there are, the higher the return is supposed to be at the end, but the volatility (risk) is also higher.

- The return on stocks and bonds (through ETF). The yield of the annualized MSCI World index over the last 20 years (2004 to 2023) is around 8.3% while the yield of the FTSE World Government Bond G7 bond index is 2.3% (backtest on Curvo website).

Using these different parameters, it is possible to simulate different scenarios and draw different conclusions. A distinction should be made between simulations made without reinvesting the tax benefits (from the federal tax and the flex income plan) and those made by reinvesting the tax benefits in ETFs.

In addition, the ETF portfolio is sold at the end of the simulation.

Simulation parameters

In our simulation, we use the following parameters:

- Investment of 1020€ entitling to the maximum tax advantage of 30%.

- Arpe pension savings fund from Argenta Bank, selected for its high performance (with no entry fees and an annual return of 6.28% between 31/12/2003 and 31/12/2023 (data retrieved from L’Echo)).

- Municipal tax of 7%.

- Employees benefiting from a flex income plan, granting them a tax advantage of €121.3 for pension savings.

- ETF portfolio composed of 70% stocks (assumed 9% annual return) and 30% bonds (assumed 4% annual return) rebalanced each year and therefore giving an assumed total annual return of 7.5%.

- TOB of 0.12% and €1 transaction fee for the broker.

- End of the simulation at the end of the year of 65 years when the last tax benefit is received.

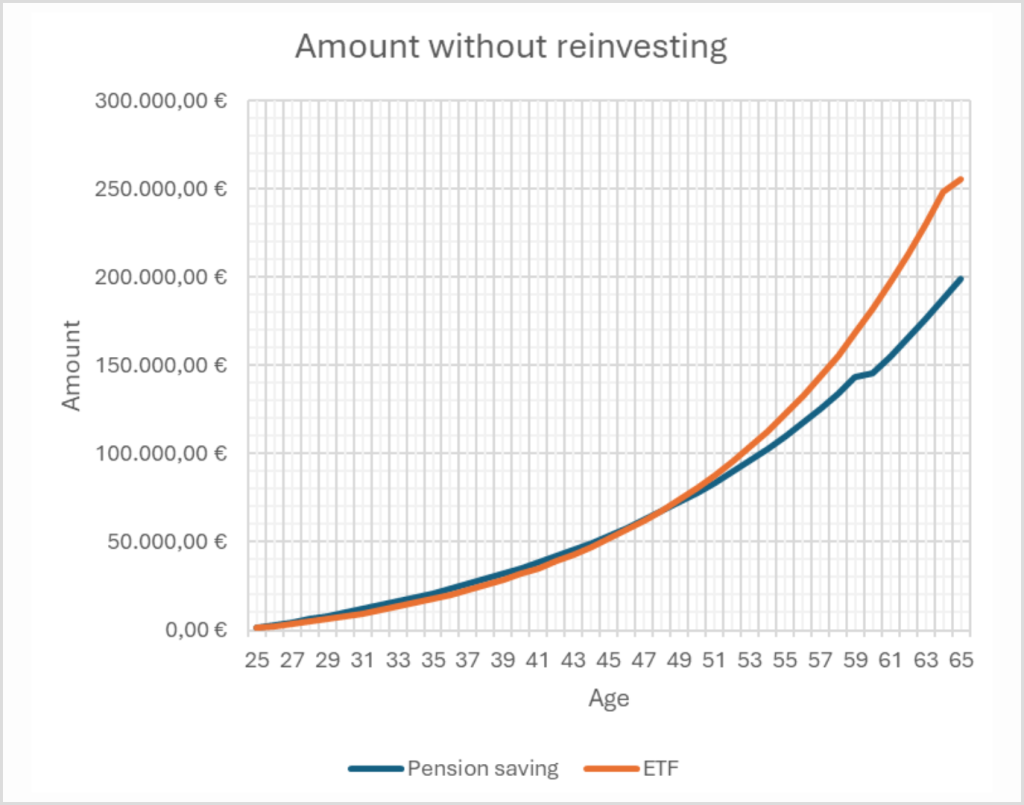

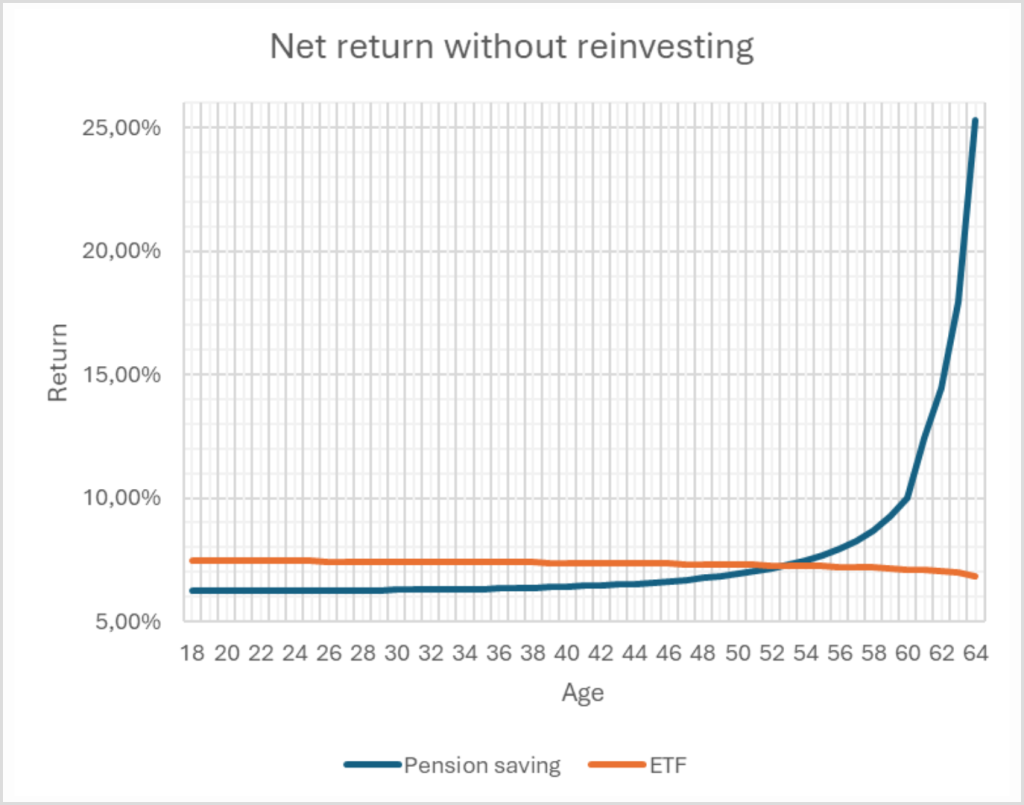

Scenario 1: without reinvesting the tax benefits.

In this scenario, it appears that investing through pension savings is advantageous only after the age of 53. The delta of amounts between pension savings and ETFs, is around €3,000.

Starting at 25 years old (40 years of deposits), the ETF portfolio performs better than the pension savings yielding around €57,000 more at the end.

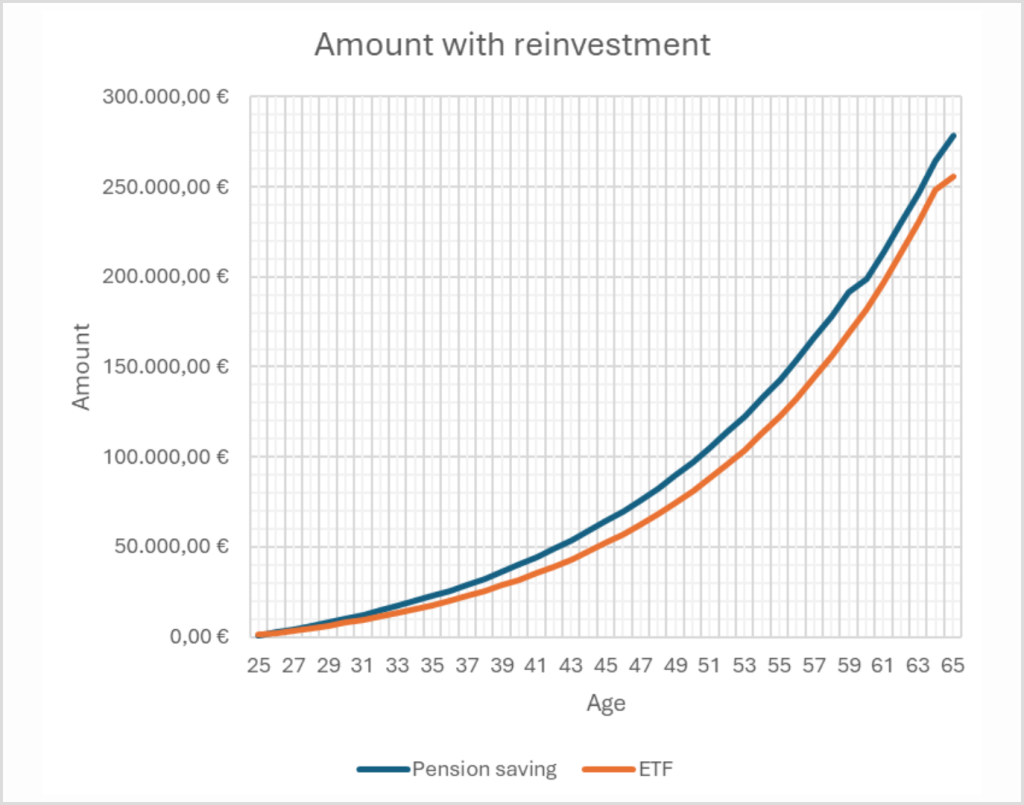

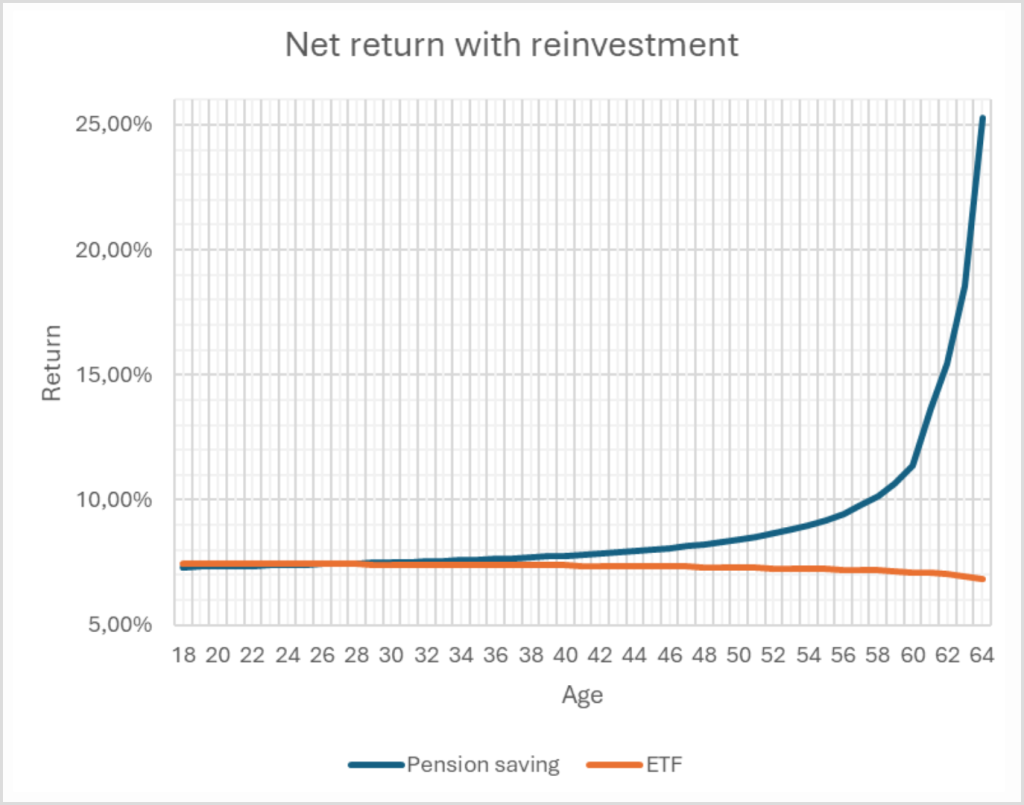

Scenario 2: Reinvesting the tax benefits into a portfolio of ETFs.

By reinvesting the tax benefits, it is advantageous to invest through pension savings from the age of 27. The delta amounts to about €22,500.

Conclusion

It is therefore advisable to check the parameters, which are unique to each person, before drawing a conclusion as to which investment is best via pension savings or ETF, and that the latter is not always more advantageous.