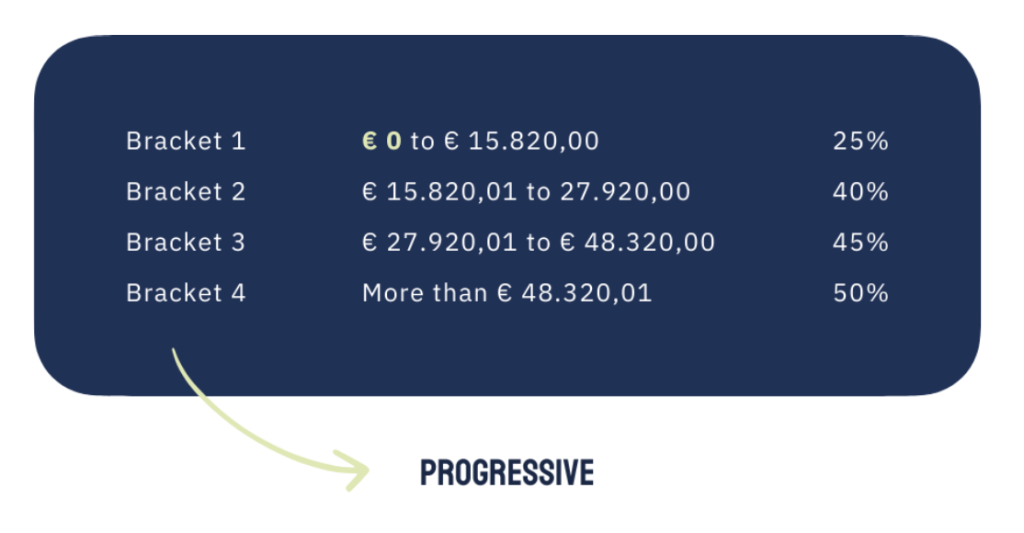

The brackets are progressive, which means that you pay a higher percentage only on the amount in that bracket, the more you earn.

There is also a tax-free allowance of €10,570, which is added to the first bracket. Depending on your situation, like how many kids you have, that allowance increases.

So, do you earn €30,000?

The difference between your tax-free allowance and €15,820 is taxed at 25%.

From €15,820 to €27,920 is taxed at 40%, and so on…

This is how you want to look at the brackets:

The moment you enter a new bracket, look for ways that have a lower tax rate than the rate of that bracket.

So let’s say you enter the second bracket. Instead of accepting the 40% on every euro that is in that bracket, take a look at the list below.

If you find something that has a lower rate, and you are eligible for it, you could consider that instead of a wage increase.

Always make sure that you are eligible before implementing. Talk to an accountant or a firm that specializes in tax optimization to verify or conduct the required research.

1. Wage (50%)

One straightforward way is through wages. Wages are subject to personal income tax, ranging from 25% to 50% based on progressive tax brackets. While taxes are unavoidable, structuring wages wisely within a tax bracket that aligns with your lifestyle needs can be beneficial.

2. Net Compensation (0%)

Certain expenses can be reimbursed tax-free. Known as net compensation, this includes necessary business expenses covered personally, such as mileage. It’s a way to extract funds without increasing your taxable income.

Summary:

- Expenses paid privately

- Strict regulation

- Business expenses

- Business trips:

- €20.8/day

- Min 6h on the road

- Max 16 days per month

- Can’t combine with Meal Vouchers

3. Meal Vouchers (Approx. 35%)

Meal vouchers provide a small but consistent tax-efficient withdrawal. The company can cover €6.91 per working day, with €2 deductible.

Summary:

- Max €8 per working day

- You pay €1.09 yourself

- Only €6.91 by company

- Of which €2 deductible

- The remaining €4.91 is a Non-Deductible Expense, which means you pay company tax on it.

- €100 => €65

4. Second Pillar Pension (Approx. 20%)

Contributing to a second-pillar pension plan reduces immediate tax liabilities and secures a future income stream. If managed correctly, this plan can serve as a long-term, tax-optimized investing route, especially if it’s allowed to grow over time.

Summary:

- Company pension plans

- Like IPT (NL) / EIP (FR)

- Long term, unless used for real estate investments.

- €100 => €80

- Some companies have the option to invest in ETFs within the IPT / EIP.

5. Liquidation Reserves (31.6%)

Liquidation reserves can be retained profits, held in reserve, and withdrawn at a lower rate after five years, effectively reducing tax impacts compared to dividends.

Summary:

- After company tax

- So it’s 20 or 25%, then 10% and then 5%

- Total = 31.6% (with 20% company tax)

- Duration is 5 years (wait time)

- Inflation kills the wait period, solutions:

- DBI = risk increase company tax

- Branche 6

- €100 => €68.4

6. Dividends (44%)

Dividends are taxed after company taxes, typically at 44%, making them relatively less attractive. However, they offer a straightforward way to profit from retained earnings if other options are maximized.

Summary:

- After company tax

- So it’s 20% or 25%, then 30%

- Total = 44%

- Immediately available

- Expensive

- €100 => €56

7. Dividends VVPR Bis (32%)

For small companies, the VVPR Bis dividends are taxed at a reduced rate of 32%. This offers significant savings for smaller firms that meet specific eligibility criteria.

Summary:

- After company tax

- So it’s 20% or 25%, then 15%

- Total = 32%

- Immediately available

- Age company must be 3+

- Beneficial

- €100 => €68

8. Warrants (Approx. 30%)

Warrants offer a flexible approach to extract funds over time. But they are also very complex to set up.

Summary:

- Before company tax!

- Immediately available (after 12 months)

- No age restrictions

- Type of “bonus” on top of your wage

- Complex

- Beneficial (especially when company tax is 25%)

- €100 => €70

9. Reconstitution Loan (Approx. 20%)

A reconstitution loan allows you to use gross revenue to buy real estate privately.

Summary:

- Pension plans as a collateral

- Buy real estate privately

- Pay with gross revenue from your company

- Funds + real estate + rent + tax reductions

- Complex

10. Share Transactions (0%)

This is an appealing option when your business gains value over time.

Summary:

- Company needs to be valuable to others

- 0% when you own the shares of your company privately

11. Copyrights (7.5% – 15%)

Copyright income, relevant for creatives, is taxed at reduced rates from 7.5% to 15%. This option suits those whose work includes intellectual property like books, media, or digital assets.

- Creation like photo, video, books, art, etc.

- Strict

- Under pressure

12. Current Account (30%)

Using your current account enables your company to borrow funds from you. While it’s an option, it may come with a 30% tax and needs a well-managed balance sheet to remain beneficial.

Summary:

- Debt you or your company has

- Only beneficial when your company has the debt

- Depends on Equity

- 2024 = 8.02%

- Beneficial when you have too much savings and don’t want to invest

13. Renting Property (Approx. 30%)

If you own a property and rent it partly to your business, the rental income can be advantageous.

Summary:

- Rent a part of your home to your company

- Calculated based on a formula

- €100 => €70

/ bryanprietoduran

/ bryanprietoduran